How to Get the Best Rate on an Auto Loan

Ever wonder how some people get such low rates on their car loans? This will tell you how to get the best rate on an auto loan—and hopefully avoid a lot of headache.

Once in a while, you'll see someone who drives a car that makes you think that they couldn't possibly afford that machine. Sometimes, it's true; they couldn't afford to pay the bills on it. However, in many cases, the reason why they can drive that car is that they know the art of getting the best rate on an auto loan.

Whether you're buying a car from a dealership or trying to get a loan to pay a private seller cash, it's crucial to know about auto loans before you try to obtain one.

A good rate can make the difference between driving an ugly used car that dies in two years and being able to afford a used car that will remain in the family for decades. Here's how to snag a great deal from lenders without losing your mind over it.

First things first—beef up your credit score.

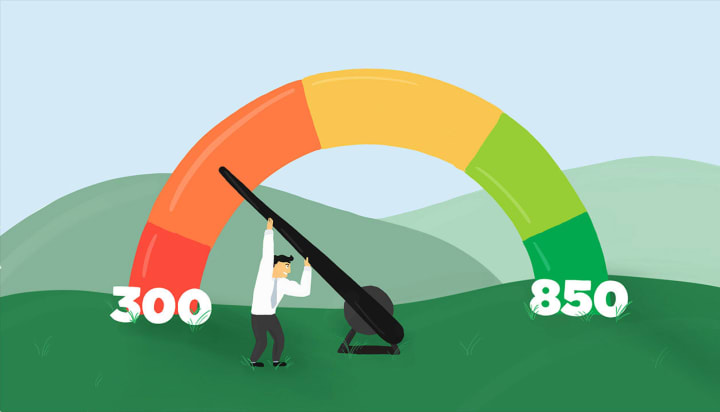

The biggest thing you need to understand about getting the best rate on an auto loan is the importance of your credit score. Your credit score is the main thing that lenders will take into account when they issue out a loan.

A credit score can be anywhere from 300 to upwards of 850. An excellent credit score typically stars around 720. (FYI, a credit score of over 720 is called "prime" by lenders and gets you the lowest rates possible.)

Credit score will make a huge impact on your auto loan rates, or any loan rate you get, really. If your credit score is below 700, you will not get a decent deal on a loan. If your credit score dips below 500, your chances of getting any auto loan are slim.

You can learn how to improve your credit score online and use sites like Credit Karma to look at your current score and file against derogatory marks on your credit report. To get a good loan, you should start doing this at least six months prior to trying to buy your car.

Don't trust the car salesman to give you the best rate on an auto loan.

A huge mistake many car buyers do is go to a car dealership that offers auto financing in hopes that they'll get a good rate. This couldn't be further from the truth in most cases.

Dealerships are businesses. Businesses need to make money. In many cases, they will fool people into paying a higher car price or paying more interest on a car loan simply because it's more profitable for them to do so.

Don't trust the dealer. The dealer is there to make a buck off of you. Do your own research.

Speaking of which, you might want to shop on your own.

Just like with finding almost anything at the best price, you need to shop around. Different banks, private lenders, and credit unions will have different rates. Such is the way things are.

If you want to get the best rate on an auto loan, you're going to have to shop around and ask different lenders what their typical interest rates and monthly payments look like.

This doesn't have to take too long; some websites allow you to enter information and get multiple bids from different groups at the same time. The important thing here is finding out what is the lowest interest rate you can get, followed by the total amount.

If you aren't 100 percent sure how much you'll need, get a prequalification from a lender. This basically allows you to get a blank check from the bank that you can use with a dealership. (The blank check is good for up to a specific amount.)

Double-check the math on your loan.

A big mistake people do is bust their butts to get the best rate on an auto loan, only to spend more money than what they saved on interest because the dealership offered a cash rebate.

A low-interest loan really isn't that good for you if you have to spend all that you saved on fees or a bloated price. Make sure you go to a dealership with good rebates if you can.

Additionally, you might want to double-check the math before you sign on the loan. Sketchy lenders will skew numbers in order to get a better cut. If the lender's math doesn't match what your calculations are, it could be that you may have agreed to terms that weren't what you thought they'd be—and that means you need to avoid signing the contract.

Research your lender and dealership.

You should never really look before you leap with financial matters, even if it's something as innocuous as getting an auto loan. A lot of the lenders say they will give you the best rate on an auto loan, only to offer loans that are riddled with fees that make it a wash.

Dealerships are not much better, and often may go so far as to make it difficult for a buyer to pay with their own money just so they can get that extra cut.

Avoid having the monthly payment talk with salesmen.

A lower monthly payment doesn't necessarily mean you got the best deal for your car loan. Your salesman probably just extended the length of the loan and raised the price. It's a common (but dirty) trick salesmen use to make you buy more car than you can really afford.

Price and lower interest rates will allow you to spend less on your car in the long run, ensuring that you get the best deal and will have extra money later on.

Don't deal with conditional loans—and focus on the price.

Conditional loans are the biggest shams that lenders and dealerships will do to customers. Basically, these are offers where they say something along the lines of, "We'll give you a loan with these terms if you buy a car that's a minimum of this price."

If the loan in question is conditional, the lender or the dealership can switch the terms around, resulting in worse terms than you initially would have been offered. Unsurprisingly, conditional loans rarely ever give decent terms to borrowers when the actual transaction comes into play.

Read the fine print at home before you buy.

Believe it or not, consumers have the right to do this before they sign on an auto loan. If your salesperson balks or demands you stay, walk out and don't go back. They are not being honest with you—or are just being too pushy for that sale.

The fine print will often tell you whether or not you're getting the best rate for an auto loan, as well as any other important rules that could impact the transaction. Above all, avoid loans that have variable interest rates or have a mandatory binding arbitration.

Contracts with variable interest rates and mandatory binding arbitration are often pretty terrible for borrowers.

Don't listen to verbal contracts.

Verbal contracts may be legally binding, but they're almost impossible to enforce. In the court of law, you will not have much luck trying to convince a judge that the salesman or lender promised you a better term than what's on the contract.

If you want them to promise anything, make sure you get it in writing. That way, you can hold them accountable for it, should they try to renege on the promise.

Up your down payment.

Last but not least, you should always remember that there are benefits to paying more upfront. A big down payment is often a good way to get better loan terms and also lower the interest rates you would be paying. In some cases, it also will allow you to get a better car than what you'd have typically been able to afford.

Sometimes, you have to spend money to save money. Such is the case with getting the best rate on an auto loan.

About the Creator

Ossiana Tepfenhart

Ossiana Tepfenhart is a writer based out of New Jersey. This is her work account. She loves gifts and tips, so if you like something, tip her!

Keep reading

More stories from Ossiana Tepfenhart and writers in Wheel and other communities.

Concept Cars We Wish Would Make It To Production

Car companies are always looking for new ways to improve their designs and engineering. The world of car design is incredibly competitive because of it, and you only need to take a quick look at the concept cars that are unveiled at auto industry shows to see that.

By Ossiana Tepfenhart6 years ago in Wheel

What Causes Your Mercedes-Benz To Jerk When Accelerating?

The engine is supposed to generate the mechanical torque required to keep your car in motion. To do that it needs a steady supply of air-fuel mixture. Besides, ignition or spark generation timing also has a significant influence on engine performance.

By Bimmer Performance7 days ago in Wheel

Impact

It was over almost before it began. Travelling up the expressway, the front left wheel buckled and twisted. The car slammed into the concrete barrier, mere inches away from my tender flesh; the only shielding a few millimetres of metal that was grinding away and some already shattered glass. My phone had gone flying from out of my pocket and was bouncing about the vehicle as my partner shrieked from the driver’s seat.

By Dave Rowlands3 days ago in Wheel

Diabolical Dealing

Charlene Lind found herself at the home of her therapist, Dr. Alexandra Vech, who she had been seeing for a week. What was supposed to be a session ended up becoming a desperate plea of help from Charlene as she was suddenly losing consciousness. She was cognizant enough to know that she had only a minute left until she would be out like a light.

By Clyde E. Dawkins7 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.